The swft blockchain settlement system is a permissioned distributed ledger built by SWIFT that settles cross-border payments in real time, 24/7, using tokenized deposits and smart-contract-enforced finality across 30+ global banks.

Key Takeaways

- SWIFT announced the blockchain settlement initiative at Sibos 2025 in Frankfurt, with 30+ banks from 16 countries co-designing the system.

- The tech stack runs on Hyperledger Besu, an EVM-compatible permissioned Ethereum client, using proof-of-authority consensus.

- An MVP with live pilot transactions is targeted for 2026, with phased production rollout expected in 2027-2028.

- Settlement times drop from 1-3 business days to seconds, with cost reductions estimated at 15-25% by removing intermediaries and manual reconciliation.

- The system interoperates with existing SWIFT rails, ISO 20022 messaging, and external networks including CBDC platforms like mBridge.

- This is the largest modernization of correspondent banking infrastructure in roughly 50 years.

1. What Is the SWFT Blockchain Settlement System?

A Next-Generation Settlement Layer for Global Banking

The settlement system is a shared digital ledger designed to record, sequence, and validate interbank payment commitments in near-real time. Unlike the legacy SWIFT messaging network, which only carries payment instructions and settles via correspondent banks over days, this new layer settles value directly on-chain. According to the official SWIFT announcement, the ledger “will extend Swift’s financial communication role into a digital environment, facilitating banks’ trusted and scalable movement of regulated tokenised value across digital ecosystems.”

From Messaging to Atomic Settlement

SWIFT has been the backbone of international payments since 1973, but it never held or moved funds. It only transmitted messages. The this type of system changes this by enabling atomic settlement, meaning the transfer of value and the associated data occur simultaneously. This hybrid approach combines SWIFT’s proven governance, security, and reach across 200+ countries with blockchain’s immutability and programmability, creating a bridge between traditional finance (TradFi) and decentralized finance (DeFi).

Why Regulated Tokenized Value Matters

At the core of the system are tokenized deposits: digital representations of commercial bank money that are fully regulated and redeemable 1:1 for fiat. By settling these tokens on a shared ledger, the system eliminates the need for bilateral nostro/vostro accounts, freeing up trapped liquidity and reducing settlement risk. The ledger is value-agnostic. Any form of regulated tokenized value, including stablecoins, tokenized deposits, and CBDCs, can circulate subject to each jurisdiction’s rules.

2. How the SWFT Blockchain Settlement System Works

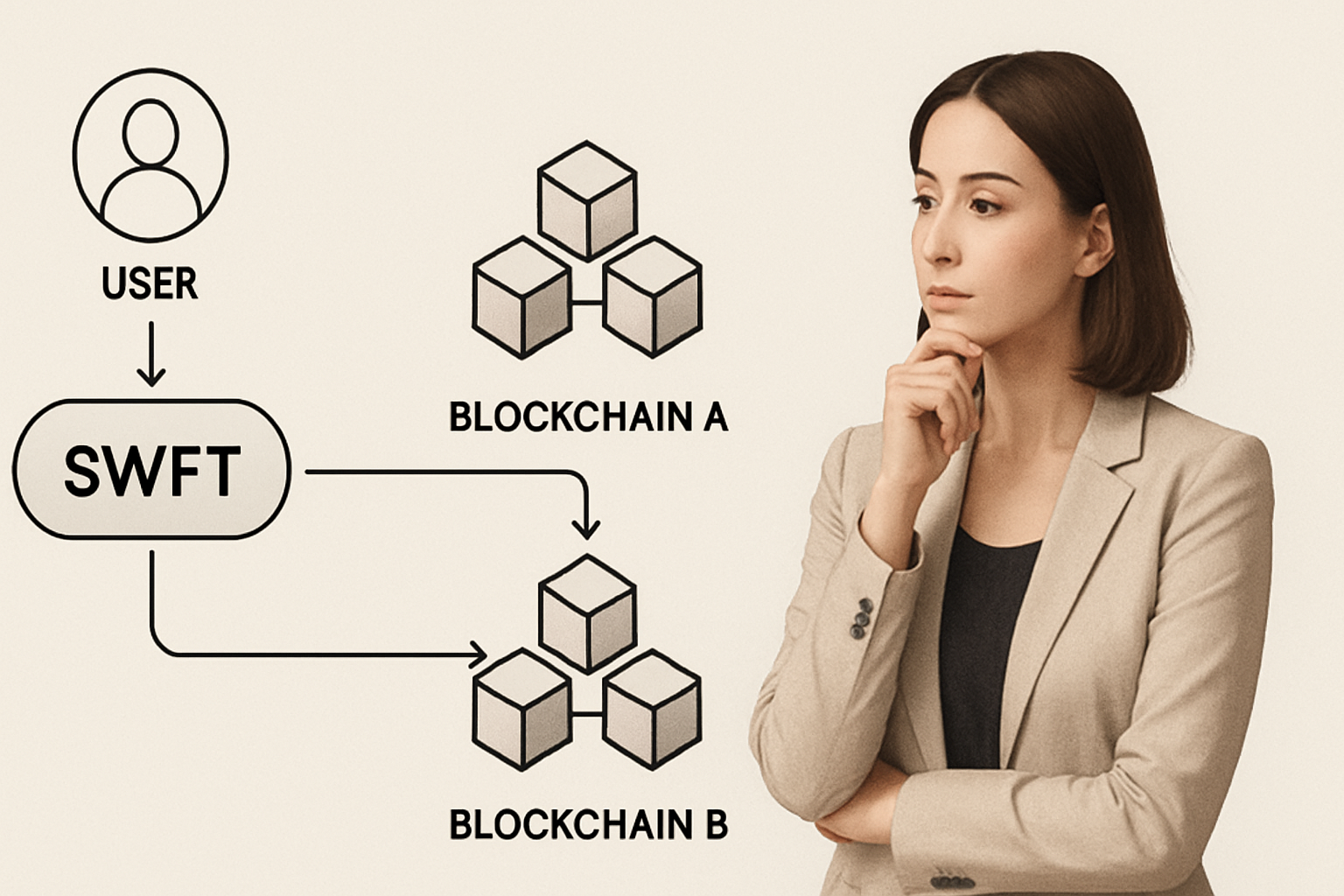

Step-by-Step Transaction Flow

- Onboarding and tokenization: A participating bank mints tokenized deposits on the shared ledger, fully backed by reserves held with a central bank or a designated custodian.

- Payment instruction: Using ISO 20022-formatted APIs, the sending bank broadcasts a payment order referencing the tokenized funds, the recipient’s wallet address, and compliance data.

- Smart-contract validation: The ledger’s smart contracts check account balances, embargo screening, AML/KYC rules, and liquidity limits. If all checks pass, the contract triggers an atomic swap of tokens and updates the ledger.

- Settlement finality: The transaction is recorded immutably across all validators. Both sides receive real-time confirmations, and the underlying fiat position is updated simultaneously via APIs into core banking systems.

- Interoperability with legacy rails: For payments involving a non-participant, SWIFT’s orchestration layer converts the token back to fiat and routes the message over the existing MT/MX network, ensuring universal reach.

Architecture and Consensus Model

The this kind of settlement system runs a permissioned Ethereum Virtual Machine (EVM) built on Hyperledger Besu, an open-source Java-based Ethereum client. According to analysis by FinTech Weekly, the choice of Besu reflects the need for “controlled governance, permissioning, compliance, predictable operations, and integration with existing bank workflows.” Consensus is achieved through a proof-of-authority (PoA) mechanism where SWIFT and a subset of trusted institutions run validator nodes, balancing performance with the accountability regulators require.

Integration with ISO 20022 and Existing SWIFT Services

A critical design principle is that the ledger does not replace SWIFT’s existing infrastructure. It augments it. SWIFT’s CEO, Javier Pérez-Tasso, stated: “Combining a shared ledger with Swift’s existing messaging, APIs and ISO 20022 creates an even more powerful construct, one that can embed risk, controls and compliance requirements from the outset into transaction flows.” Banks can continue using familiar FINplus and GPI interfaces while gradually adopting the blockchain settlement rail.

3. Key Features and Benefits of the SWFT Blockchain Settlement System

Real-Time 24/7 Settlement

Traditional correspondent banking operates on a 5-day-a-week, batch-based schedule, with settlement often taking 1-3 business days. The the blockchain settlement system processes transactions continuously, cutting settlement time to seconds. This always-on capability is essential for e-commerce, instant remittances, and treasury operations that require liquidity around the clock.

Tokenized Deposit Efficiency

By representing fiat as programmable tokens, banks can automate liquidity management. Tokenized deposits reduce reliance on prefunded accounts and allow intraday credit to be allocated dynamically. The IEEE paper “SWIFT is Preparing to add a Blockchain to manage cross border payment settlement process” (IEEE Xplore) suggests that blockchain integration could lower settlement costs by 15-25% by removing intermediaries and manual reconciliation steps.

Enhanced Security and Compliance

Every transaction on the system is cryptographically signed and immutably recorded. Smart contracts encode regulatory rules, including anti-money laundering checks and sanctions screening, at the protocol level. No payment can bypass compliance checks. The PoA consensus, combined with SWIFT’s existing Customer Security Programme, creates a defense-in-depth posture that protects against fraud and cyberattacks.

Global Reach Across 200+ Countries

SWIFT connects more than 200 countries and territories. The blockchain settlement layer inherits this network effect, meaning a bank in Singapore can settle directly with a bank in Argentina without building new bilateral relationships. The interoperability solutions announced alongside the ledger ensure that even banks not yet on the blockchain can still receive payments via the legacy rails.

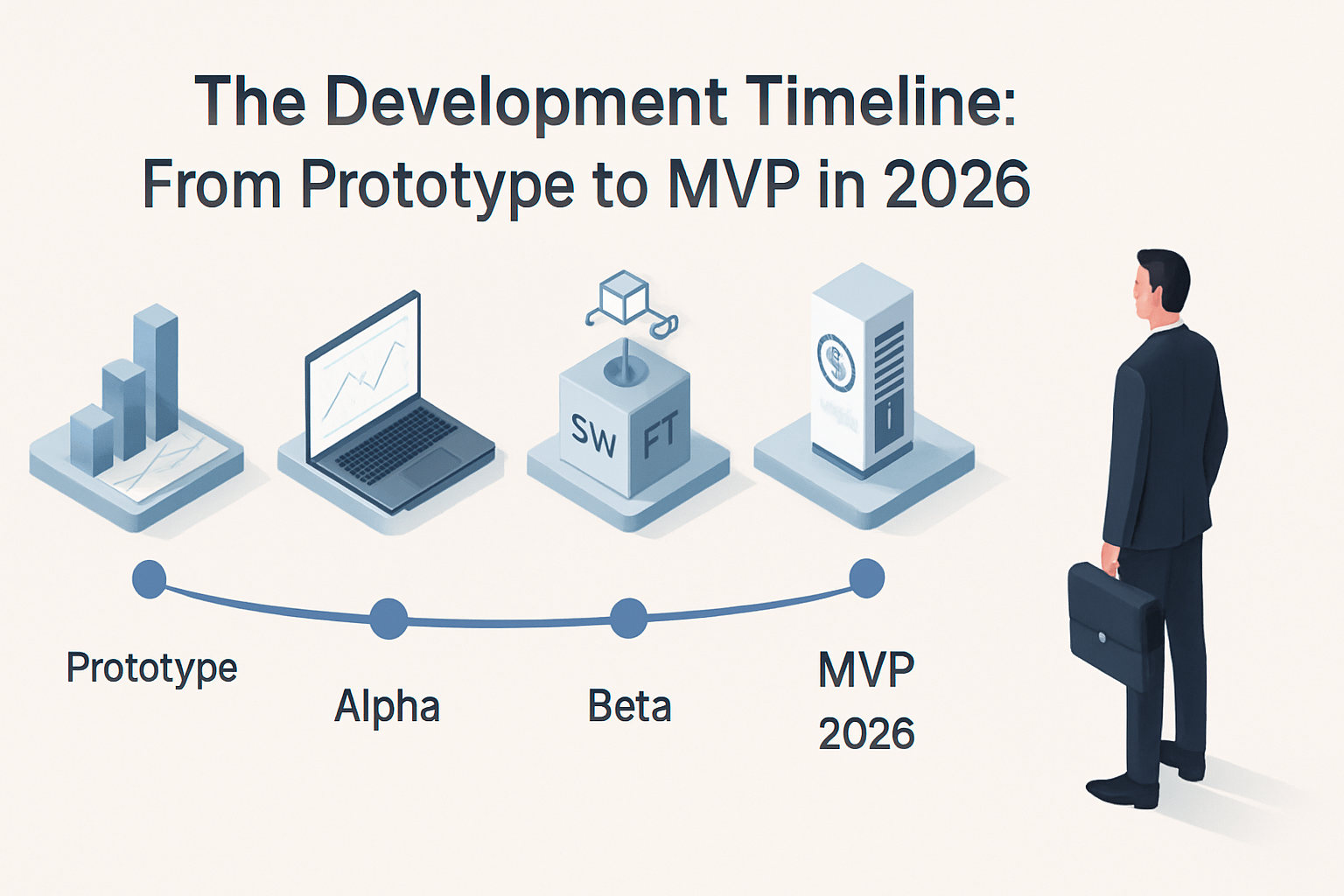

4. The Development Timeline: From Prototype to MVP in 2026

Phase One: Conceptual Prototype with Consensys (September 2025)

SWIFT announced the initiative at Sibos 2025 in Frankfurt, revealing a collaboration with Consensys to build a conceptual prototype. This phase focused on validating the architecture, defining smart-contract standards, and gathering input from the advisory group of 30+ banks. Key milestones included successful lab tests of atomic settlement between tokenized USD and EUR positions.

Phase Two: Minimum Viable Product and Pilot (2026)

On March 30, 2026, SWIFT confirmed that the design phase was complete and that an MVP was under construction. According to FinTech Weekly, “SWIFT has set an ambitious pace, with plans to initiate a pilot program within this year.” A select group of participating banks will begin executing real-value transactions in a controlled environment, testing interoperability with domestic instant-payment systems like TIPS in Europe and FedNow in the United States.

Full Production Rollout (2027-2028)

No official production date has been announced, but industry observers expect a phased live deployment starting in late 2027, gradually onboarding all 11,000+ SWIFT-connected institutions. The rollout will likely coincide with broader adoption of tokenized deposits and regulatory clarity around blockchain-based settlement in key jurisdictions such as the EU, the UK, Singapore, and Japan.

5. Participating Banks and Industry Collaboration

The 30-Plus Founding Banks

The breadth of support for this initiative is significant. Financial institutions from 16 countries are providing feedback on the design, including:

- Bank of America

- BNP Paribas

- Citigroup

- Deutsche Bank

- HSBC

- JP Morgan Chase

- MUFG

- Santander

- Standard Chartered

- Wells Fargo

- Additional institutions listed in SWIFT’s press release.

This coalition represents a critical mass of global transaction banking volume, giving the system the liquidity depth it needs from day one.

Voices from the Community

“We hope that Swift will introduce a scalable blockchain solution and enable us to provide our customers with uninterrupted, 24/7 real-time settlement.”

“No single institution can achieve this alone. Swift’s neutral role and global network uniquely position it to drive industry collaboration.”

Technology Partners

Beyond Consensys, SWIFT is working with infrastructure providers like Chainlink for external data oracles, and multiple cloud and security vendors to ensure the ledger meets the stringent uptime and resilience requirements of systemic financial market infrastructure.

6. Technology Stack: Hyperledger Besu and Ethereum Compatibility

Why Hyperledger Besu?

Hyperledger Besu is an open-source Ethereum client designed for enterprise use. It supports both public and permissioned networks, offers high throughput via parallel transaction execution, and includes native privacy features such as private transactions and node-level permissioning. The system uses Besu’s EVM compatibility, meaning any developer familiar with Solidity can build compliance or liquidity applications on the network without learning a new execution environment.

Permissioned vs. Public Blockchains

Many have asked why SWIFT did not simply use the public Ethereum mainnet. The answer lies in the specific requirements of regulated finance: controlled validator sets, deterministic finality, predictable gas costs, and integration with legacy core banking systems. As Galvin Lee Kuan Sian of Taylor’s College explained to FinTech Weekly, the system “requires controlled governance, permissioning, compliance, predictable operations, and integration with existing bank workflows.” The EVM-compatible design borrows Ethereum’s developer ecosystem while keeping governance in SWIFT’s hands.

Smart Contracts as the Enforcement Layer

Smart contracts on the system serve two purposes: transactional logic and compliance automation. For a simple payment, a contract verifies that the sender’s ISO 20022-formatted instruction includes all required fields, then atomically swaps tokens. More complex contracts can facilitate Delivery-vs-Payment (DVP) for securities, or trigger conditional payments based on IoT data, opening up entirely new trade-finance use cases. Below is a simplified illustration of what a settlement validation contract might look like in Solidity:

// SPDX-License-Identifier: MIT

}

}

"Compliance check failed"

}

}

In production, the compliance oracle would connect to SWIFT’s AML/sanctions screening layer via Chainlink or a similar external adapter, keeping sensitive data off-chain while enforcing rules on-chain.

7. SWFT Blockchain Settlement System vs. Ripple and Other Alternatives

Comparative Landscape

| Feature | SWFT Blockchain Settlement System | RippleNet / XRP Ledger | JP Morgan Onyx / JPM Coin | Traditional SWIFT GPI |

|---|---|---|---|---|

| Network type | Permissioned consortium (PoA) | Public/permissioned hybrid (XRP Ledger) | Permissioned (Quorum) | Centralized messaging |

| Settlement asset | Regulated tokenized deposits | XRP (bridge currency), stablecoins via partners | JPM Coin (tokenized USD) | Central bank reserves (via correspondents) |

| Settlement time | Seconds (real-time 24/7) | 3-5 seconds | Near-real-time (intra-day) | 1-3 business days |

| Global reach | 200+ countries (inherited from SWIFT) | 55+ countries (300+ financial institutions) | Limited to JPM clients | 200+ countries |

| Compliance model | Embedded in smart contracts | Via partner nodes and external checks | JPM-enforced KYC/AML | Bilateral agreements and screening |

| Consensus mechanism | Proof-of-Authority (SWIFT and member nodes) | XRP Ledger Consensus Protocol (UNL) | Quorum’s Raft-based consensus | N/A |

Sources: SWIFT press release, FinTech Weekly, Ripple.com, JP Morgan Onyx documentation.

Why Not Ripple?

Ripple has been a pioneer in blockchain-based settlement, but the swft blockchain settlement system offers a different value proposition. It is deeply integrated with the existing correspondent banking framework, requires no bridge currency (FX conversion can happen on-ledger or via external channels), and carries the weight of SWIFT’s governance and compliance regime. For most banks, this is a more gradual path to blockchain adoption than switching to an entirely new network.

Complementarity, Not Competition

SWIFT has explicitly stated that its ledger will interoperate with other networks, including public and private blockchains. This points toward a future where the system acts as a hub connecting domestic instant-payment systems, CBDC networks, and DLT-based trade platforms, creating a true internet of value.

8. Governance, Tokenomics, and Validator Structure

How Validator Nodes Are Governed

Governance of the swft blockchain settlement system sits with SWIFT as the network operator, with participating banks running validator nodes under contractual obligations. Unlike public blockchains where anyone can propose protocol upgrades, changes to the settlement rules, smart-contract logic, or consensus parameters go through SWIFT’s existing governance bodies. This gives regulators a clear accountability chain, which is a prerequisite for systemic financial market infrastructure designation in most jurisdictions.

Tokenized Deposit Issuance and Redemption

Tokenized deposits on the ledger follow a strict mint-and-burn model. A participating bank mints tokens against verified fiat reserves, transfers them on-chain during settlement, and the receiving bank redeems them against its own reserve position. No token circulates without a corresponding fiat liability, which means there is no speculative token economy here. This is not a cryptocurrency. It is a programmable representation of regulated bank money, and that distinction matters enormously for regulatory treatment under frameworks like the EU’s MiCA regulation and the UK’s Digital Securities Sandbox.

Interest and Liquidity Mechanics

One open question is whether tokenized deposits will accrue interest while in transit. Traditional nostro balances do not earn interest, which is a significant drag on bank profitability. If SWIFT’s design allows tokenized deposits to remain interest-bearing during the settlement window, even for seconds, it could meaningfully improve the economics of correspondent banking. The protocol documentation has not yet specified this definitively, and it will likely vary by jurisdiction based on central bank policy.

9. Challenges and Regulatory Considerations

Regulatory Fragmentation

Tokenized deposits are still a novel concept in many jurisdictions. The system must navigate a patchwork of laws governing money transmission, digital assets, privacy (including GDPR), and capital requirements. SWIFT has engaged regulators globally, but harmonized standards for tokenized liabilities are years away from being finalized.

Scalability and Performance

SWIFT processes approximately 44 million messages daily. Even with permissioned Besu’s optimizations, sustaining that throughput on-chain is a significant engineering challenge. The solution will likely shard by currency corridor or region, and rely on a settlement-bus pattern where netted batches are committed to the ledger while the underlying messages flow separately.

Adoption by Smaller Banks

The 30-plus design partners are mostly global tier-1 institutions. Smaller banks, particularly in emerging markets, may lack the technical expertise and capital to run validator nodes or integrate with the ledger. SWIFT is exploring sponsor models in which larger banks validate on behalf of smaller correspondents, but this could reintroduce concentration risks that regulators will scrutinize carefully.

Competing CBDC Initiatives

Several central banks are developing their own wholesale CBDC platforms. Project mBridge, involving the central banks of China, Hong Kong, Thailand, and the UAE, is the most advanced multi-CBDC settlement network currently in operation. Project Agorá, a BIS-coordinated initiative involving 7 central banks, is exploring tokenized commercial bank money on a shared ledger, which overlaps directly with SWIFT’s approach. The swft blockchain settlement system must coexist and interoperate with these sovereign networks, which could limit its role to a private-sector overlay rather than the foundational settlement layer in some corridors.

10. The Future of Cross-Border Payments with SWFT Blockchain

Impact on Global Commerce

Businesses will be able to send and receive cross-border payments instantly, reducing working capital tied up in transit. According to a Ripple report cited by FinTech Weekly, banks invested more than $100 billion in blockchain infrastructure from 2020 to 2024, and 90% of finance leaders expect blockchain to have a major impact on finance by 2028. The swft blockchain settlement system is positioned to capture a significant portion of that investment wave as the most credible institutional-grade settlement rail.

Opportunities for Fintech and Infrastructure Providers

“For investors, the opportunity is in the infrastructure layer that makes this possible,” Maghnus Mareneck of Cosmos Labs told FinTech Weekly. This includes companies providing connectivity between ledgers, compliance tooling, treasury management interfaces, and tokenization-as-a-service platforms. The emergence of this settlement infrastructure will accelerate demand for these adjacent services, creating a new ecosystem of regulated DeFi products. If you are building in this space, the Digital Blockchains studio is actively working on protocol infrastructure and tokenomics design for exactly these use cases.

The Convergence of TradFi and DeFi

Bill Zielke, Chief Revenue Officer at BitPay, told FinTech Weekly: “The real story isn’t TradFi vs. crypto, but their convergence. From here, what drives real adoption is how well they connect and how invisible the seams are.” As regulated tokenized deposits become commonplace, consumers and businesses will experience a financial system that is always on, borderless, and programmable, without ever needing to know the blockchain underneath. For a deeper look at how tokenized assets are reshaping settlement infrastructure, see our analysis of tokenized assets on blockchain.

Pros and Cons

Pros

- Real-time 24/7 settlement cuts transaction times from 1-3 business days to seconds, improving liquidity for all participants.

- Inherited network reach across 200+ countries means no new bilateral relationships are required for most corridors.

- Compliance embedded at the protocol level via smart contracts reduces manual screening overhead and audit costs.

- EVM compatibility allows existing Solidity developers to build on the network without learning a new stack.

- No bridge currency required, unlike RippleNet, which eliminates FX exposure to a volatile intermediary asset.

- Broad institutional backing from 30+ tier-1 banks across 16 countries provides immediate liquidity depth.

Cons

- Centralized governance under SWIFT and a small validator set raises questions about censorship resistance and single points of failure.

- Regulatory fragmentation across 200+ jurisdictions will slow adoption in markets without clear tokenized-deposit frameworks.

- Scalability at 44 million daily messages remains an unproven engineering challenge for any permissioned EVM chain.

- Smaller banks face high barriers to running validator nodes, potentially concentrating network control among tier-1 institutions.

- Competition from CBDC projects like mBridge and Project Agorá could fragment the settlement landscape rather than unify it.

Frequently Asked Questions

What is the SWFT blockchain settlement system?

The swft blockchain settlement system is a permissioned distributed ledger being built by SWIFT to settle cross-border payments instantly using tokenized deposits and smart contracts, while maintaining full regulatory compliance. It is co-designed with 30+ global banks from 16 countries and targets an MVP launch in 2026.

When will the SWFT blockchain settlement system go live?

The MVP is expected to launch with live pilot transactions in 2026, with a phased production rollout likely in 2027-2028 for the broader SWIFT network of 11,000+ connected institutions. No official production date has been confirmed as of mid-2026.

Which banks are involved in the SWFT blockchain project?

Over 30 global banks from 16 countries are co-designing the system, including Bank of America, BNP Paribas, Citigroup, Deutsche Bank, HSBC, JP Morgan Chase, MUFG, Santander, Standard Chartered, and Wells Fargo. The full list is available in SWIFT’s official press release.

How does the SWFT blockchain settlement system differ from Ripple?

Unlike RippleNet, the SWFT system does not require a bridge currency like XRP, is deeply integrated with existing SWIFT messaging and correspondent banking relationships, and embeds compliance directly in smart contracts. For most regulated banks, this makes adoption significantly smoother than migrating to an entirely new network.

Is the SWFT blockchain settlement system secure?

Yes. It uses Hyperledger Besu with proof-of-authority consensus, embedded compliance smart contracts for AML and sanctions screening, and inherits SWIFT’s Customer Security Programme standards. Every transaction is cryptographically signed and immutably recorded across all validator nodes.

Can non-SWIFT members use the blockchain settlement system?

Initially, only SWIFT members will participate directly. The interoperability layer converts tokens back to fiat and routes payments over legacy MT/MX rails for non-participants, ensuring universal reach from day one without requiring every institution to join the blockchain network immediately.